))

The Future of Energy - Small Modular Reactors (SMRs) and How to Invest

Manage episode 444948483 series 3586928

Contenido proporcionado por Dominic Frisby. Todo el contenido del podcast, incluidos episodios, gráficos y descripciones de podcast, lo carga y proporciona directamente Dominic Frisby o su socio de plataforma de podcast. Si cree que alguien está utilizando su trabajo protegido por derechos de autor sin su permiso, puede seguir el proceso descrito aquí https://es.player.fm/legal.

Quick heads up. I have made some video versions of recent articles. Here they are, in case you are a watcher rather than a reader:

I don’t know about you, but I use artificial intelligence (AI) all the time. ChatGPT has become my right-hand man. It gives me advice (really – and good advice too), it helps me make decisions, it gives me exercise workouts, recipes, it proofreads what I write, it helps me write titles, it even helps me write song lyrics. Midjourney does all the imaging for this newsletter. Even a simple Google search now involves lots of AI.

I know I’m not alone. Almost everyone is using AI, consciously or not.

Guess what? AI requires bucket loads of power. That’s why Microsoft recently agreed to pay Constellation Energy, the new owner of America’s infamous nuclear power station, Three Mile Island, a sizeable premium for its energy. There is cheaper wind and solar power to be had in Pennsylvania, but it isn’t as reliable as nuclear, 24 hours a day.

It’s not just AI. The widespread political desire to rid ourselves of fossil fuels means the world needs electricity, and fast.

Nuclear is the solution, of course. But nuclear takes a lot of time, even with AI now “re-routing” the anti-nuclear narrative. It takes especially long in the UK where any kind of infrastructure project requires billions to be spent on planners, lawyers and consultants before a brick is even lifted.

It’s so stupid of course. Nuclear power stations have been operating commercially for 70 years, providing reliable, affordable, and almost infinitely renewable “clean” electricity. Nuclear has the best safety record of any energy technology. Almost all environmental concerns, such as waste disposal, have been solved. But if you want to know the name of the point at which stupidity, hypocrisy, waste and weakness meet, it’s called British Energy Policy.

Layer upon layer of safety is demanded in nuclear plant design. The regulatory process is slow, cumbersome, and complex. There is a long lead time between planning, building, and operation, which adds to expense. Political uncertainty meant many proposals for nuclear power stations in the UK were shelved. It all drives away investment.

But governments around the world are waking up to the fact that the silver bullet is nuclear-powered. Thus, the narrative is changing. The dawn of the new age of nuclear power is upon us, and it can’t come quickly enough.

That’s why the focus has shifted to small modular reactors (SMRs). These have been operational for almost 70 years now in submarines, aircraft carriers, and ice-breakers, but in the last few years, land-based SMRs have been developed to generate electricity.

They use simple, proven technology, and are safer than current nuclear power stations. They can be manufactured in factories and then rapidly erected on-site. Modular refers to the design principle of breaking down a system into small, independent, and interchangeable components, or “modules”, that can easily be combined, modified, or replaced without affecting the rest of the system. This flexibility means they are scalable. It aids manufacture, transportation, and installation while reducing construction time and costs.

SMRs don’t occupy much land, so they have little impact on the landscape. Some can even be constructed underground – surely preferable to wind turbines and solar farms. In the UK, they could be erected on the redundant sites of closed nuclear and coal-fired power stations, where grid connections are readily available.

A 440 megawatt (MW) SMR would produce about 3.5 terawatt hours (TWh) of electricity per year, enough for 1.2 million homes – or to provide power to Wales, the Northeast of England, or two Devons. It would require about 25 acres of land. A solar farm would need 13,000 acres for the same output; a wind farm, 32,000 acres. Three 440MW SMRs would be enough for London, which has around 3.6 million homes.

What’s more, their output is not dependent on the weather. Reliability is why Microsoft paid a premium of more than 85% for Three Mile Island’s power. SMRs produce electricity that can easily be adjusted to meet the constant, everyday needs of the grid (baseload), and they can also ramp up or down to follow changes in demand throughout the day. They spin in sync with the grid, so they help keep everything stable. When they’re running, they act like a steady hand, providing momentum that makes it easier to manage sudden changes in electricity supply or demand.

Why not subscribe to this amazing publication?

How To Invest

There are all sorts of ways to invest in nuclear power. The simplest and least risky is to buy the metal itself. Current demand for uranium stands at around 200 million pounds per year, while mining output totals only 140 million pounds. Another 25 million pounds comes from secondary sources, such as scrap and recycling. So there is a uranium supply deficit. I’m surprised the price isn’t higher. London-listed Yellowcake (LSE:YCA) has been set up with this purpose in mind. It is, essentially, a uranium holding company. You buy the shares, and thus own a share of the uranium it holds. It makes up part of the Dolce Far Niente portfolio.

You could also buy uranium miners, though I have to say I do not like the miners at all. There are the large producers, such as Cameco (Toronto: CCO) and Paladin Energy (Sydney: PDN). You can also gain exposure via large caps, such as Rio Tinto (LSE: RIO), but they are not pure plays. There are mine developers too, such as NexGen Energy (Toronto: NXE), whose Rook 1 project should be producing a whopping 30 million pounds a year by 2030, almost enough to solve the uranium supply deficit single-handedly.

If you don’t fancy your stock-picking skills, go for a fund instead. The London-listed Sprott Uranium Miners ETF (LSE: URNP) is an exchange-traded fund that gives you exposure to a basket of mining companies, as does closed-end fund Geiger Counter (LSE: GCL). Another popular ETF is the Global X Uranium UCITS ETF (LSE: URNU).

Why don’t I like uranium miners? About 90% of those listed in the funds do not have any production coming in the near future and are, therefore, huge vortexes into which capital will disappear. At present, they are fully valued. That’s not saying they won’t go up. But when the time comes for them to fall, they will bomb.

When I last looked at SMRs in 2021, the companies I tipped were Rolls-Royce (LSE: RR) and Fluor Corp (NYSE: FLR). Both have been real winners. Rolls-Royce has built seven generations of SMRs for use in nuclear submarines and, with its modern designs for SMRs, has been winning contracts all over. Rolls-Royce is not a pure SMR play. But it has put its SMR business into a separate entity (Rolls-Royce SMR) and I presume this will be spun out and listed at some later stage.

The stock has been going great guns under its new CEO, Tufan Erginbilgiç. I tipped it around the 100p mark and it’s now at 530p and there’s no stopping it. It was 1,350p in 2013, so there’s plenty of upside left, and that was before there was any urgency about SMRs. I’ve taken my original stake off the table, and the rest I’m holding.

I also mentioned NuScale, a US outfit, which in 2021 was unfortunately still private. There was a way to get exposure to NuScale, however: via majority shareholder and engineering company Fluor Corp. It has been a real winner too. We tipped it at $18. It’s now $50. The stock remains a hold, although it is not a pure play. Worth $8.6bn, Fluor has $200m of free cash flow and trades at 42 times earnings.

But the company we were looking at, NuScale Power Corporation (NYSE: SMR), has now listed – good ticker – and you can buy the stock at not far off the flotation price. Be warned, however: this is a volatile company. Since its initial public offering (IPO) at $10, the stock has been as high as $15 and as low as $2. It is now at $13.

NuScale designs, develops, and commercialises SMR reactors for nuclear-power generation, aiming to provide a “safe, flexible, and scalable nuclear-energy solution”. Its flagship product is the NuScale Power Module, a self-contained pressurised water reactor (PWR) that is far smaller than traditional nuclear reactors. Each module has an electric capacity of about 60 megawatts, but they can combine to scale up.

NuScale has partnered with various organisations, including the US Department of Energy (DOE) and global energy firms, but it does not yet have a solid sales pipeline, so it is hard to value. Instead, it’s a bit of a meme stock that rises and falls when it gets tipped. NuScale has a market capitalisation of $1.2bn and revenues of $23m; it lost $273m last year. It now has $180m in negative free cash flow, $130m in cash and a burn rate of about $35m per quarter. (So it’s got enough money for another year.) Caveat emptor.

Another option is BWX Technologies (NYSE: BWXT), but again it’s not a pure SMR play, more of a picks-and-shovels play. The company manufactures nuclear-reactor components, systems fuel, and other critical parts for the nuclear-power industry. It really is wide-ranging (think anything from naval nuclear propulsion to nuclear defence) and its history goes all the way back to the Manhattan Project.

SMR developers will often rely on BWX’s expertise and manufacturing capabilities to ensure the safety and functionality of their designs. As demand for SMRs grows, so will the appetite for BWX’s products and services. BWX has a market value of $10bn and $1.2bn in debt. Earnings per share are just shy of $3, and the price/earnings (p/e) ratio is close to 40. But it is profitable and pays a yield just below 1%.

If you want to go really small and speculative, there is always the mining exploration option (not recommended), or uranium enrichment firms. If this technology of enriching uranium to make it more powerful comes good, then the efficiencies of the industry will improve even further, and the problem of uranium supply deficits will quickly vanish, along with the high prices of many uranium miners. Silex Systems (Sydney: SLX) – market cap A$1.1bn (£565m), 50% owned by Cameco – is the market leader here, although Centrus Energy (NYSE: LEU), worth $1bn, is not far behind.

We are still some years from successful enrichment, but it is coming. I doubt we will see it before the uranium price itself breaks to new highs above $140/lb, which it hit in 2006, and probably not until $200 uranium. High prices have a habit of accelerating everything. Uranium is now at $70/lb.

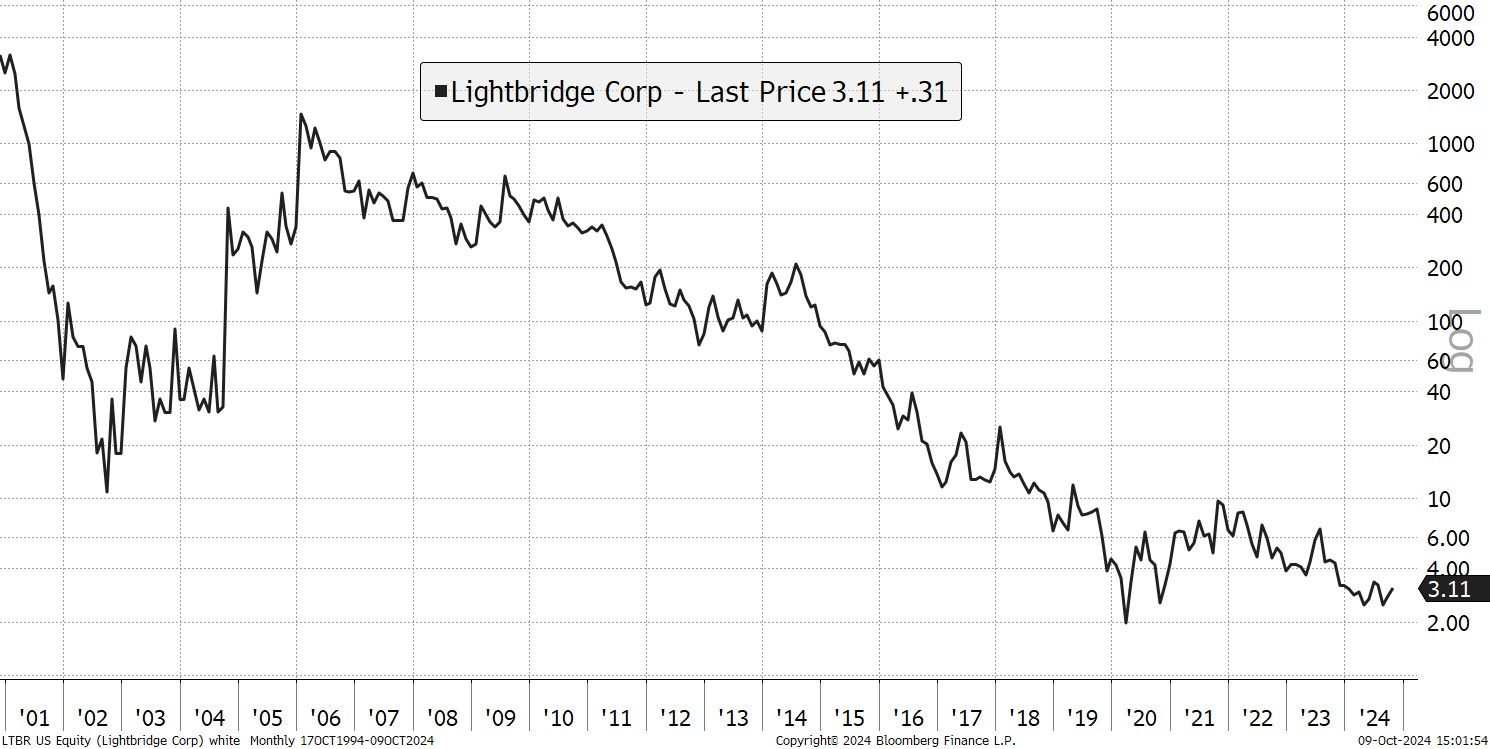

That’s when tiny-cap nuclear-fuel tech firms such as Lightbridge (Nasdaq: LTBR), worth $46m, could rocket. Lightbridge, looking to improve the safety, economics, and proliferation resistance of nuclear power, is developing a fuel that operates about 1,000 degrees cooler than standard fuel. It’s got $27m in the bank, is losing $10m a year and, like NuScale, seems to rely on memes and tipsters. The stock costs $3 so there is plenty of upside. But be warned: this is an illiquid Nasdaq stock. Don’t chase it.

Amazing chart. From $4,000 - to $2. Talk about wealth destruction. It’s like an NHS IT project. Looks like it might, finally, have bottomed though.

This article first appeared in Moneyweek Magazine.

I’ll be MCing this year’s Moneyweek Summit on Friday November 8th. Readers of the Flying Frisby can get a 20% discount by entering the code FRISBY20

If you’re interested in nuclear, Wednesday’s piece might be of interest:

I had an email from Nick Lawson, CEO of investment house, Ocean Finance, which has put together some research on Lightbridge. I share it here, in case of interest.

And here once again are those vids:

19 episodios